Key Takeaways:

- The number of Parents using Target’s app are down 17.5% Y/Y, hitting a 14-quarter low.

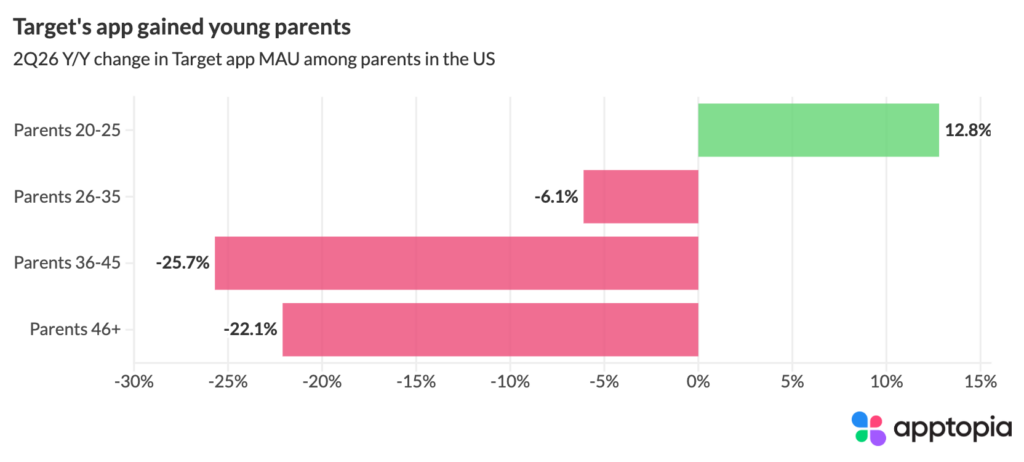

- The percentage of all parents who used Target’s app at least once this month grew 12.8% Y/Y among parents aged 20–25, its only growing cohort. The percentage among parents aged 36–45 fell 25.7%.

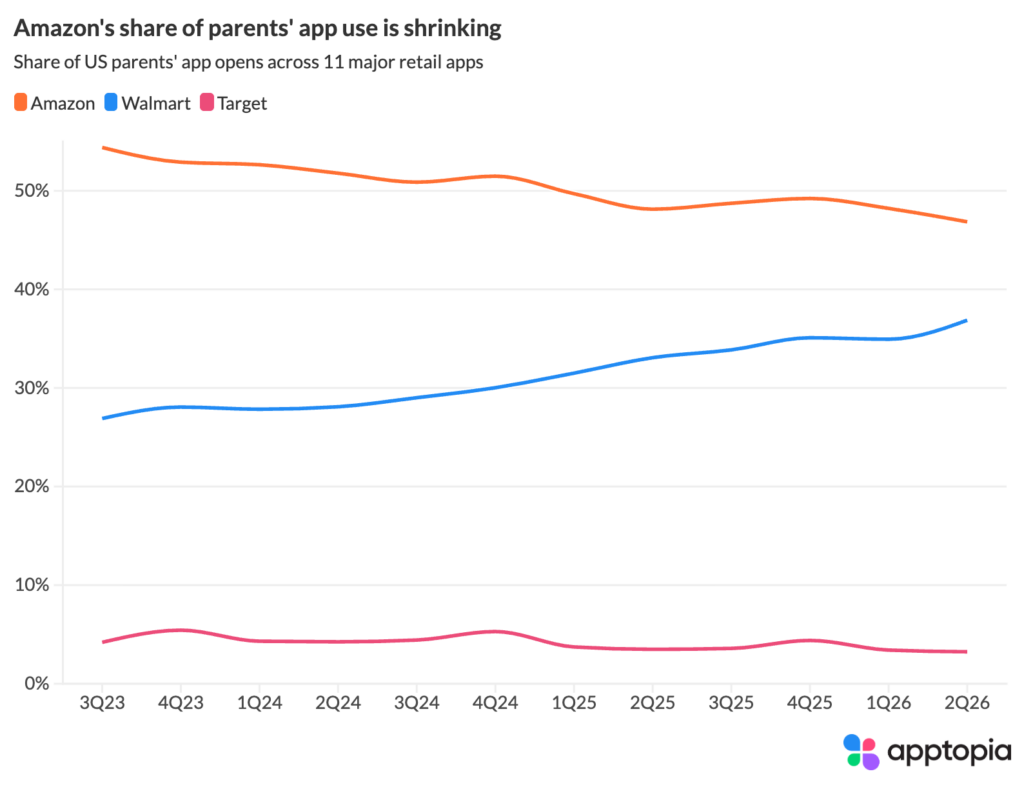

- Looking at a grouping of eleven top retail apps, Walmart now captures 37% of parents’ retail app opens (up from 25% in 2023), while Amazon’s share slipped below 47% for the first time.

Target [NYSE: TGT] finally handed the Street a quarter it could work with in May. Comparable sales grew 5.6%, the first positive print in five quarters, traffic rose 4.4% and full-year guidance went up. The stock fell anyway, because one good quarter against soft compares proves momentum, not durability. The fiscal second quarter, which closes August 1, is where the turnaround thesis gets tested. Apptopia’s panel data on parents, the customer Target has explicitly said it needs back, offers an early read. Most of it is uncomfortable. One piece of it is the most encouraging signal Target has produced in this dataset.

Start with why parents matter. In March, Target began rolling out baby boutiques in roughly 200 stores, its largest investment in the category in over a decade, stocking UPPAbaby strollers and Stokke high chairs next to the diapers. The logic came from Target’s own research: when consumers become parents, they consolidate where they shop. Win the stroller purchase and the grocery trips follow. The urgency came from the scoreboard. Numerator data cited by CNBC shows Target’s share of the baby category slid from 18.6% to 17.6% over two years while Walmart’s grew.

Our data says the consolidation is still running the wrong way. Among all parents in Apptopia’s US consumer device panel, Target’s MAU penetration hit 6.7% in 2Q26, the weakest quarter in a series that runs back to the start of 2023, and down 32% from its 4Q24 peak. The year-over-year decline of 17.5% lands against a 2Q25 comp that already carried the damage from last spring’s consumer boycotts. Target is comping down against a bad quarter. The erosion is steepest exactly where the franchise used to be strongest, with MAUs among parents aged 36 to 45 falling by a quarter in a single year.

Then there is the age gradient: Year over year, MAUs among parents 20 to 25 rose 12.8%. The 26 to 35 cohort slipped 6.1%. The 36 to 45 group fell 25.7%, and parents over 46 dropped 22.1%. The younger the parent, the better Target’s app performed. That youngest cohort had posted four straight quarters of year-over-year declines before flipping positive in 2Q26, the first full quarter the baby boutiques were on the floor. Their session activity in the app grew 25% over the same period. One quarter of data from the panel’s smallest cohort does not prove the boutiques caused the inflection. It does show the exact demographic the strategy was built for turning up in the exact quarter it arrived, while every other cohort headed the other direction.

“Baby is a category retailers underwrite on lifetime value, so the cohort Target is winning is the one that can compound,” said Tom Grant, VP of Research at Apptopia. “If those new parents consolidate their spending the way Target’s own research says they do, this quarter’s MAU numbers becomes the next decade’s comps.”

Pooling sessions across eleven retail apps, Walmart [NASDAQ: WMT] has grown its share of parents’ retail app activity from 25% to 37% since early 2023. Amazon [NASDAQ: AMZN] surrendered the most ground, about 7 points, dropping below 47% of the pool for the first time, with eBay [NASDAQ: EBAY] giving up another 3 points and Target roughly 1. Walmart’s parent penetration sits at 38.2%, a 5.7x multiple of Target’s. Nobody would call that distress; Walmart just reported transaction growth at its highest level in six quarters. But at the margin, something shifted. Walmart’s growth among parents 17 to 25 decelerated from 17.5% year over year in 1Q26 to 3.2% in 2Q26, the same quarter Target’s youngest cohort inflected. Among the newest parents, momentum moved in Target’s direction for the first time in this dataset.

Below the giants, the middle of American retail is losing parents outright. Kohl’s [NYSE: KSS], Macy’s [NYSE: M], and JCPenney combined reached 4.0% of parents in early 2023. That figure now stands at 2.5%, down 25% in the past year alone, and Walmart’s app reaches fifteen times as many parents as all three department store apps put together. Kohl’s shows the sharpest decline in our set of studied apps, off 27% year over year to a series low, with penetration among parents 36 to 45 down 38%. That is the core customer CEO Michael Bender’s back-to-basics revamp is built to recover, and it makes for a rough early read on a company whose CFO told analysts in March that traffic remains the central problem. Costco [NASDAQ: COST] is running the opposite arc, with the fastest growth among parents since 2023 at +60%, now decelerating. Millennial parents aged 26 to 35 is the only cohort still growing for the app.

eBay [NASDAQ: EBAY] slipped below 10% of parents for the first time in the series, down 14% year over year, but the decline is entirely an older-parent phenomenon. Parents 46 and up, eBay’s largest cohort, fell 18%, while parents 20 to 25 grew 7% and posted their strongest second quarter in the data. A new parent outfitting a nursery on a stretched budget is the natural ecommerce customer, and eBay has spent years courting exactly that positioning. The pattern holds beyond those two: in every major retail app in the file except Costco, parents 17 to 25 were the best-performing cohort in 2Q26, while parents over 35 declined at all of them. At Target and at eBay, the youngest parents moved against the grain of every cohort above them. The newest generation of parents looks up for grabs in a way established parents do not.