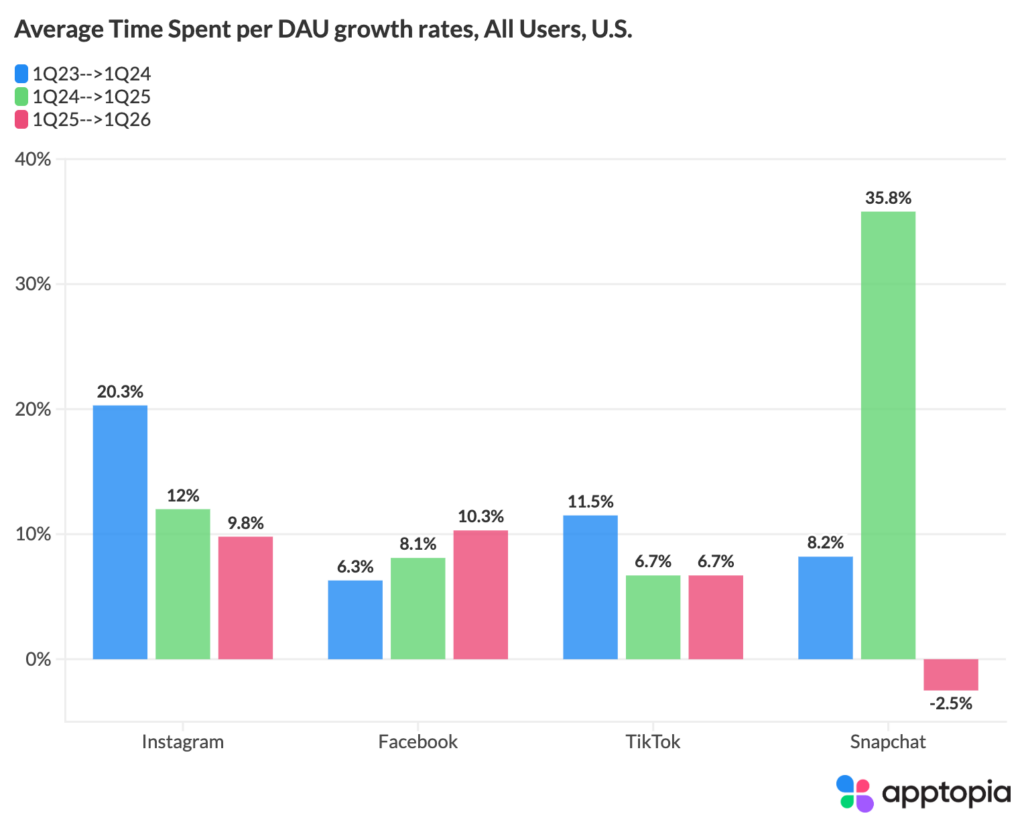

Every quarter, we look at average time spent per daily active user across major US social platforms using Apptopia’s consumer device panel. The Q1 2026 data stands out for one reason: three of four platforms grew engagement year-over-year. Snapchat didn’t.

Comparing Q1 2025 to Q1 2026, Instagram [NASDAQ: META] grew Average Time Spent per DAU by 9.8%. Facebook grew 10.3%. TikTok grew 6.7%. Snapchat [NYSE: SNAP] declined 2.5%.

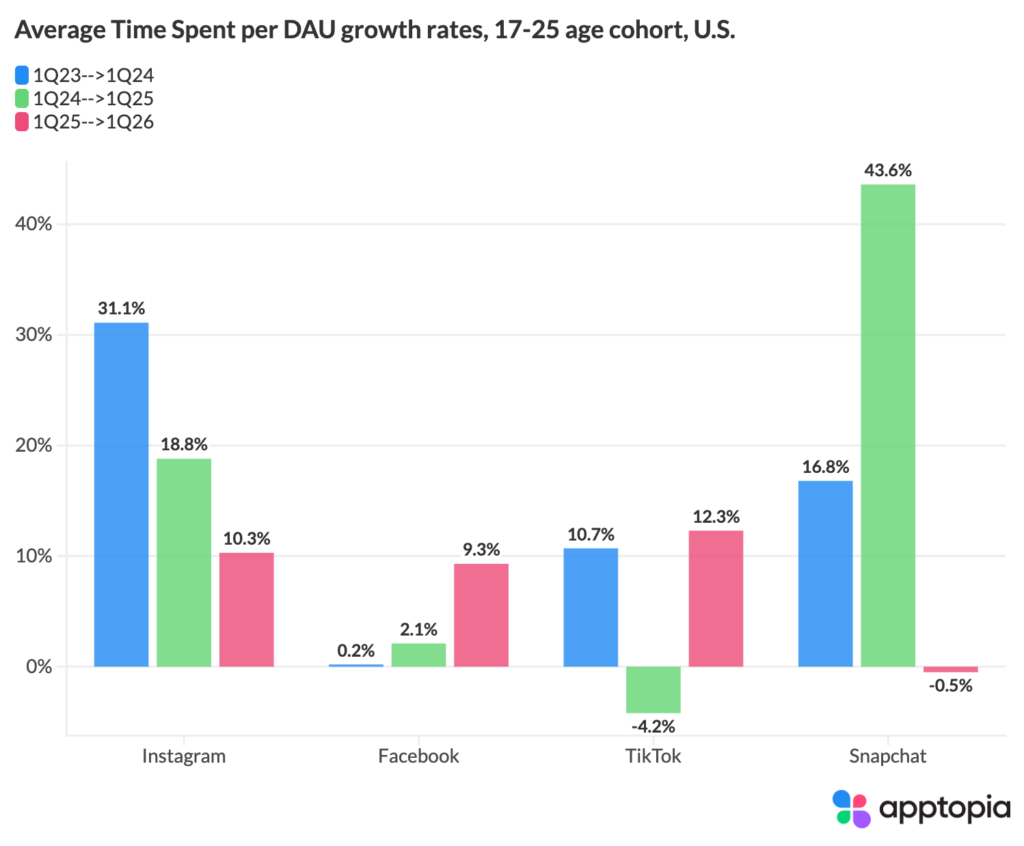

That alone would be notable. What makes it more significant is where Snap was twelve months ago. Q1 2025 was the strongest first quarter in Snap’s recent history on this metric. Time spent surged 35.8% versus Q1 2024. The 17-25 cohort, Snap’s core franchise demographic, spiked 43.6%. The product was gaining traction across every age group.

Q1 2026 reversed nearly all of it. The 17-25 cohort went from +43.6% to -0.5%. The 26-35 group went from +21.6% to -0.4%. Full-year 2025 data confirms Snap carried momentum through the middle of the year; annual growth was 16.0% for all users, meaning the reversal is recent.

The wider pattern is just as telling. Over the three Q1 periods in our study, Snap’s time spent growth rates were 8.2%, then 35.8%, then -2.5%. That’s a 38pp spread between the highest and lowest readings. Facebook’s equivalent spread was 4 points (6.3%, 8.1%, 10.3%). TikTok’s was 5 points. Instagram’s was 10.5 points, decelerating gradually from a high base. Snap is the outlier on consistency by a wide margin. Its average Q1 growth of 13.8% looks similar to Instagram’s 14.0%, but the path is a spike and a crash versus a steady glide. For anyone building a forward estimate around Snap’s engagement trends, that volatility is the problem. You can underwrite a growth rate that compounds quarter after quarter. You can’t underwrite one that swings 38 points.

“When one platform reverses while the rest of the sector keeps growing, it’s not something macro going on,” said Tom Grant, VP of Research at Apptopia. “If Gen Z were broadly pulling back from social apps, you’d see it everywhere. You do not. So not only is SNAP seeing a Q1 decline while others rise, it is now experiencing rising volatility as a business.”

The rest of the competitive set held up. Facebook posted its third consecutive Q1 acceleration, with growth concentrated in the 26-45 age range — the highest-CPM demographic in digital advertising. Instagram grew across every cohort, led by 26-35 at 14.1%. TikTok still commands the most absolute time per user in every age group, roughly 2x Facebook and 2x Instagram, and its time spent growth of 6.7% was positive if unspectacular.

Time spent across major social platforms continues to grow (time spent on mobile as well), but the consistency of that growth increasingly separates the pack. For investors, the Q1 data suggests the more durable engagement stories right now sit with Meta and TikTok, while Snap’s trajectory remains the one that needs the most proving out.