Match Group (MTCH) is navigating a significant top-of-funnel cooldown with company-level downloads plunging 25.4% QoQ so far in 2Q26. Despite this acquisition pressure, the company is still fighting to keep an even keel when it comes to DAU growth, which is -0.1% QoQ so far.

While Tinder’s downloads and DAUs mirror what is happening at the company level, Hinge is somewhat of a bright spot so far. Here’s what Apptopia’s mobile signals are showing for MTCH.

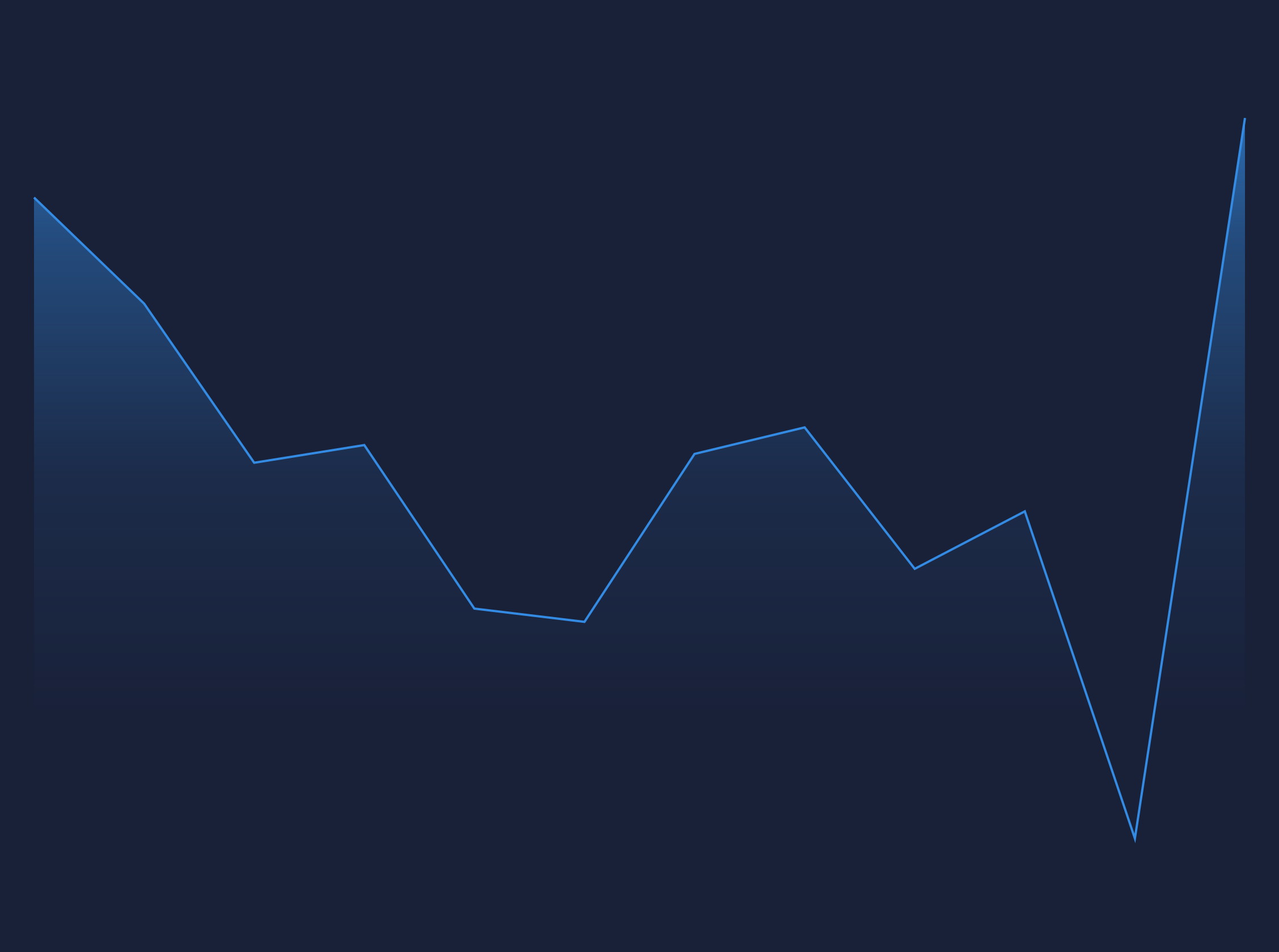

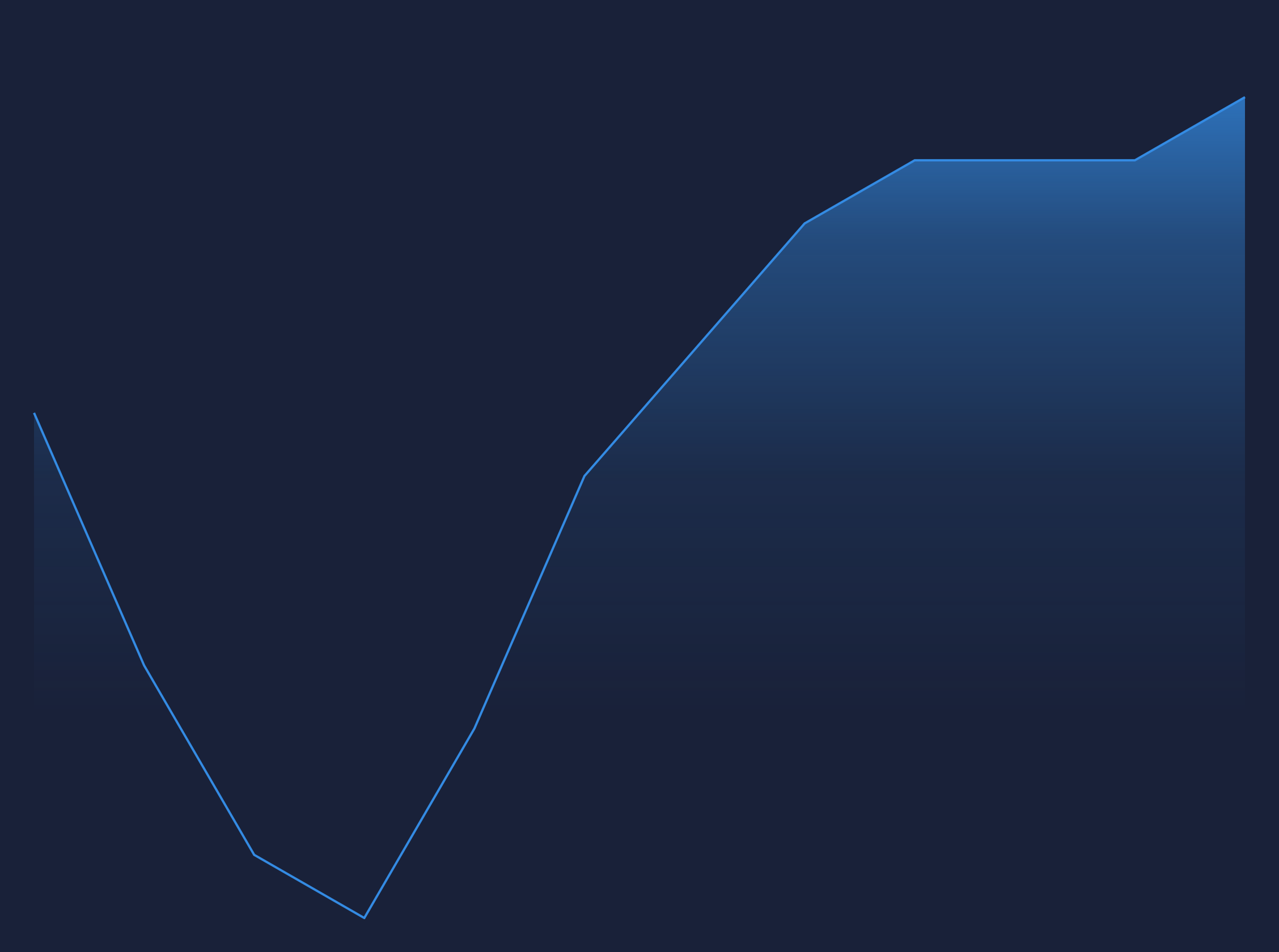

Downloads Retreated to 3.4M (-25.4% QoQ)

For the week of April 13, Match Group’s downloads reached an estimated 3.4M, representing a sharp -25.4% QoQ decline and a -2.5% WoW dip. While downloads remain up 4.6% YoY, the significant quarterly retreat signals a cooling in top-of-funnel momentum as the company moves into Q2 2026. This softening in new-user intake puts added focus on the behavior of the existing installed base.

This drop in downloads suggests that Match needs to pivot from growth-led scale to engagement-led stability. Rotating the company’s focus to user retention may support steadier near-term monetization even if top-of-funnel pressure continues to temper the long-term growth outlook. Feel free to reach out to discuss how we analyze retention with Apptopia’s data.

Engagement Trends

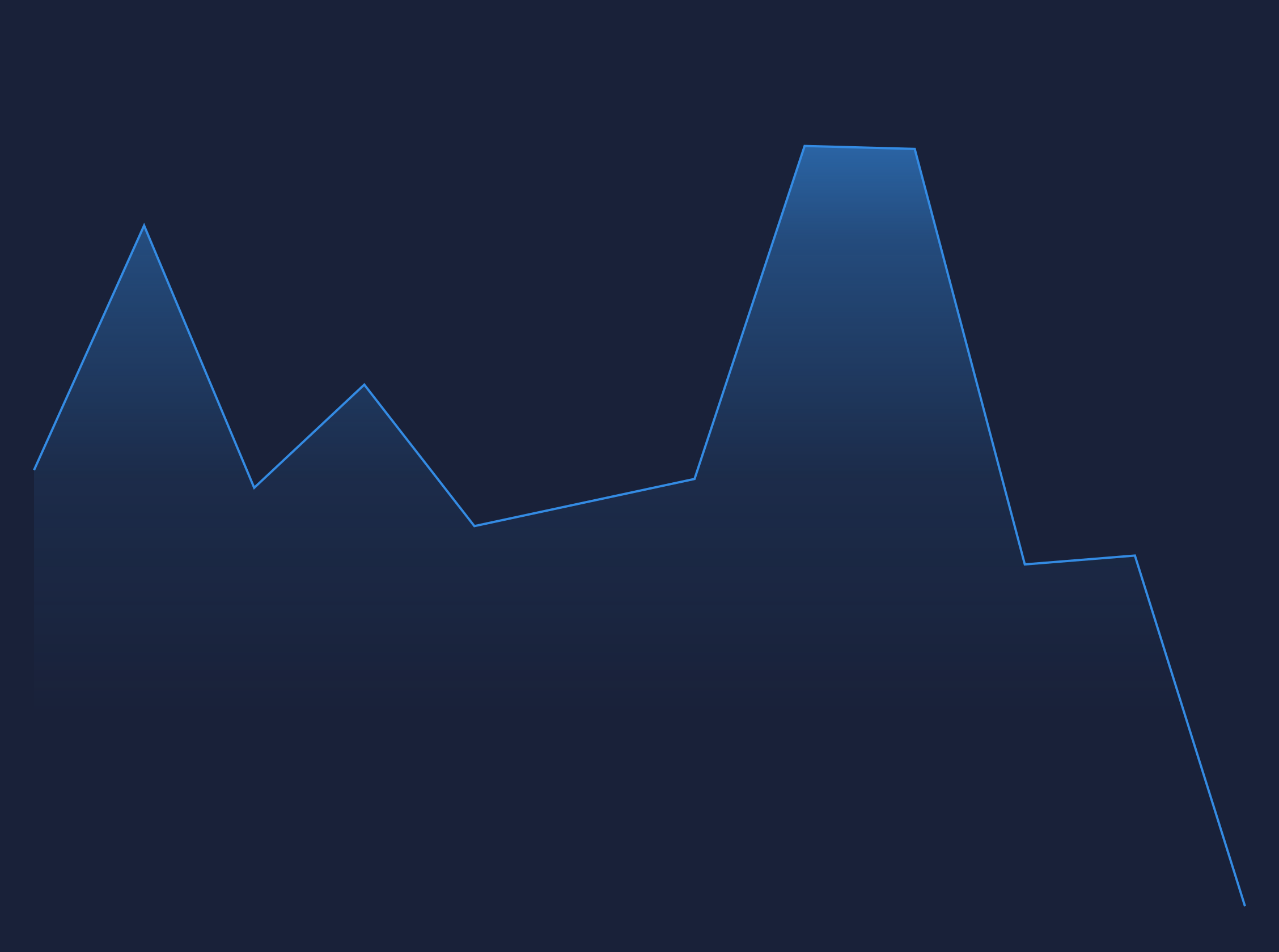

In Q1 2026, Match Group’s estimated DAU reached 62.6M, representing a strong 8.0% YoY increase and a 1.4% QoQ gain. This growth in daily active users, alongside a 2.5% YoY rise in MAU to 280.3M, suggests deeper daily penetration within the existing footprint despite the slowdown in new downloads.

For the week of April 13, DAU held essentially flat at an estimated 62.6M (-0.1% WoW). This steady weekly performance indicates a resilient platform footprint at the aggregate level. While per-app intensity remains mixed, the sustained YoY growth in daily users suggests that Match Group is successfully transitioning toward a more engaged, “sticky” user base to drive monetization.

Retention Quality Appears Relatively Healthy

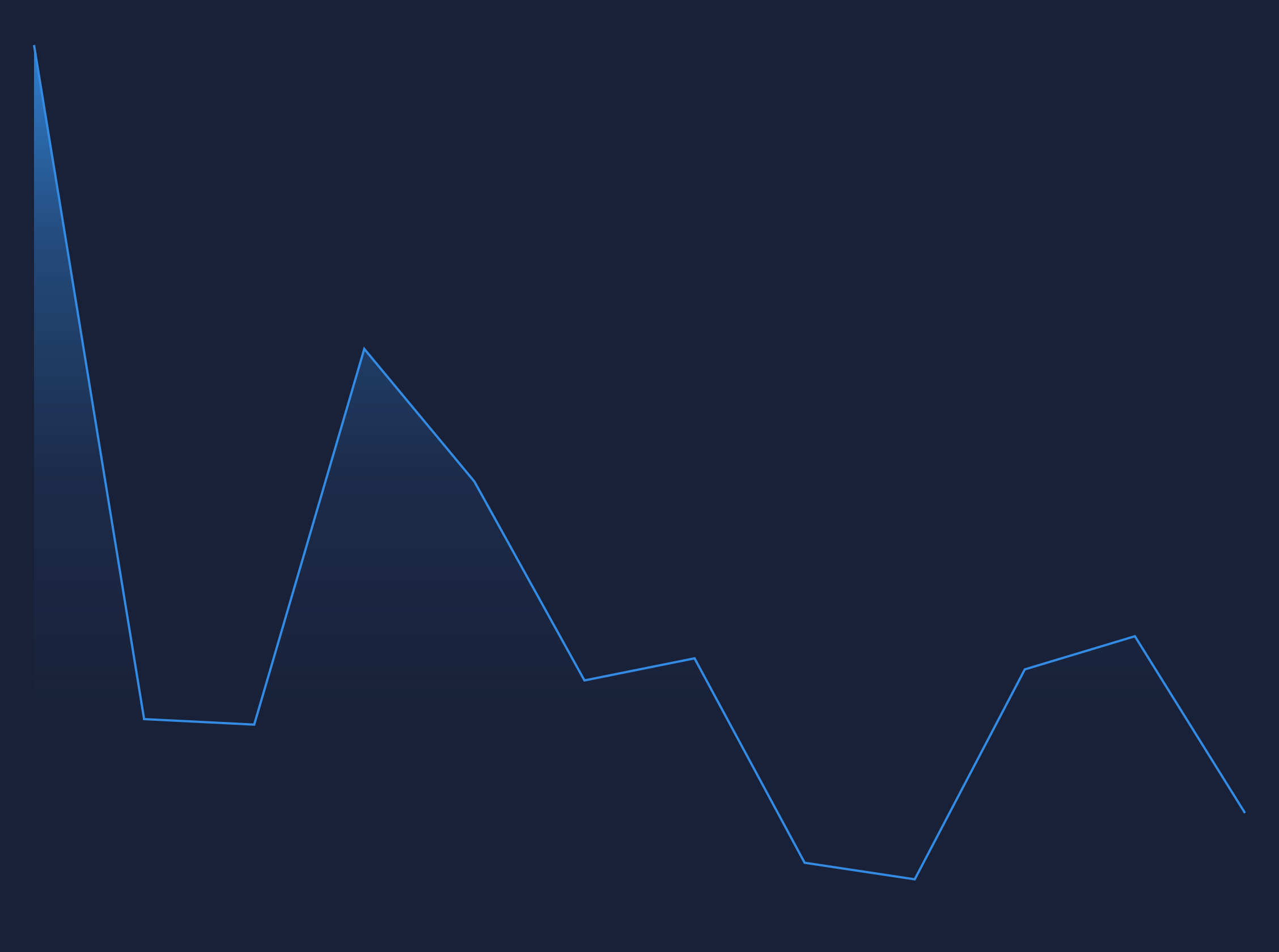

Match Group’s core brands demonstrate a resilient but varied attrition profile, led by Tinder’s estimated churn of 33.3%. While Hinge’s churn sits slightly higher at 41.0%, the portfolio average remains competitive.

For investors, Tinder’s sub-40% churn typically correlates with strong recurring revenue visibility and efficient CAC payback. Despite the broader slowdown in new-user acquisition, the aggregate stability across these high-value brands suggests that Match Group is successfully retaining its most monetizable users.

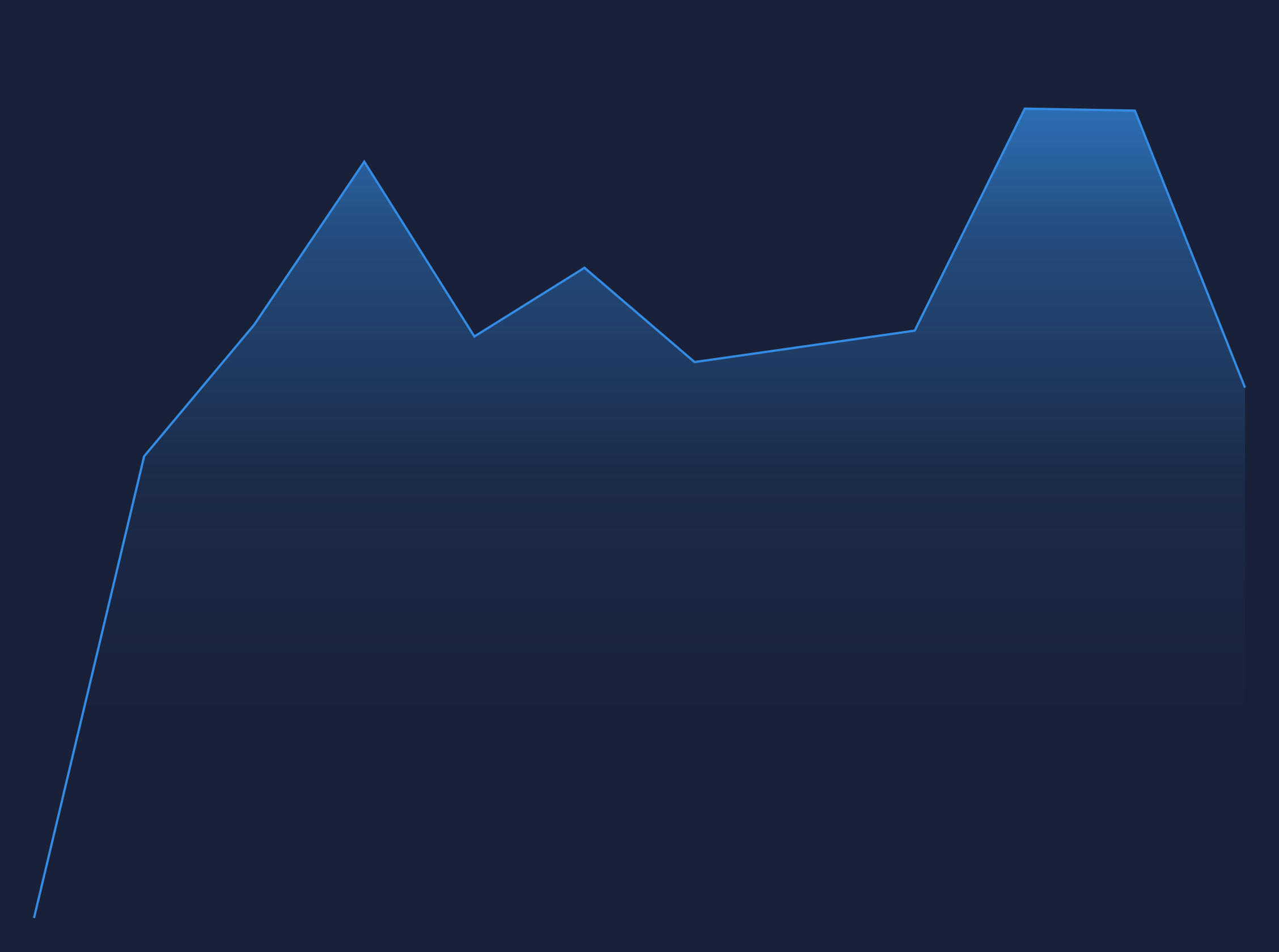

Mixed Mobile Signals Heading Into Q2 2026

Match Group’s mobile metrics show a mixed profile heading into Q2 2026. Declining MPI and softer acquisition suggest weaker momentum, while stable DAUs and low churn indicate a still-resilient base.

Apptopia’s data provides a useful lens for monitoring whether this divergence between top-of-funnel pressure and steadier engagement persists into Q2 2026.

Investors should use Apptopia’s metrics to track whether download softness, mixed engagement intensity, and healthy retention continue to shape Match Group’s near-term trajectory.