Apptopia leveraged its US consumer device mobile panel to determine how major airlines are performing with different age groups. All data in this post is focused on Sessions, also known as app opens. The study period is from Q1 2024 through Q1 2026. Airlines in the Legacy bucket are United [NASDAQ: UAL], American [NASDAQ: AAL] and Delta [NYSE: DAL]. Airlines in the LCC/Hybrid bucket are Southwest [NYSE: LUV], JetBlue [NASDAQ: JBLU] and Alaska [NYSE: ALK].

Older users dominate overall engagement. The 46+ age group accounts for 43.5% of total airline app sessions across all carriers, nearly four times the 10.6% share contributed by the 17–25 cohort. The relationship is monotonic: engagement climbs steadily through the 26–35 bracket (20.1%) and 36–45 bracket (25.8%) before peaking with the oldest users.

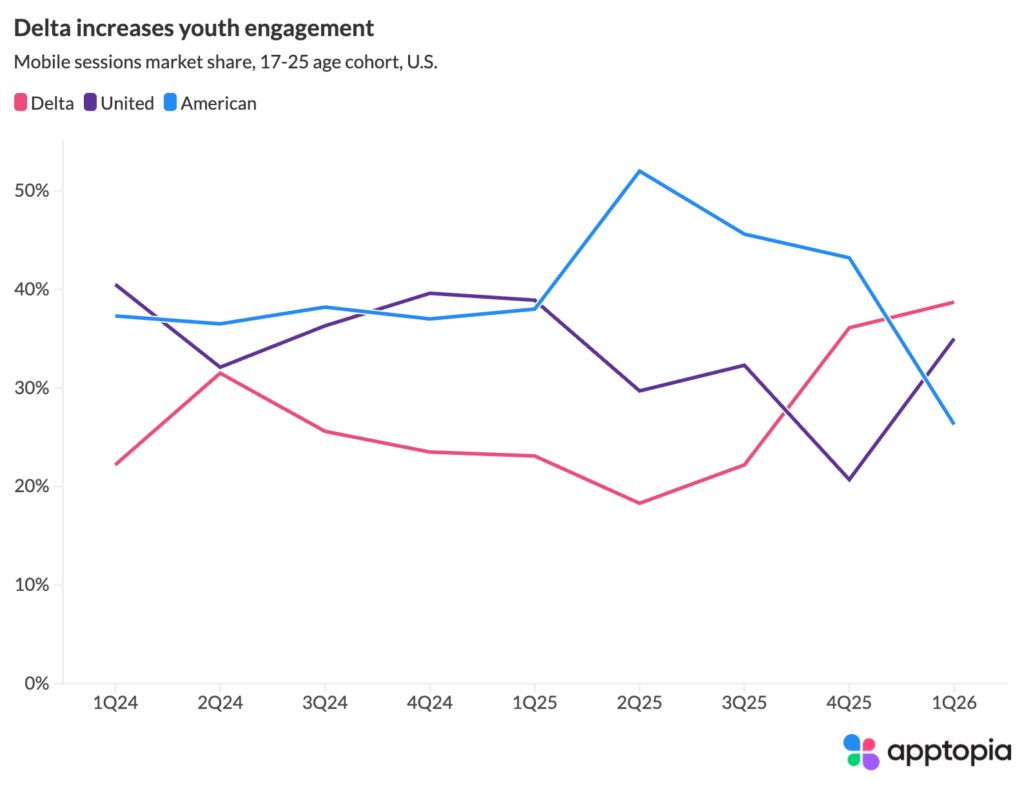

The Legacy Market: A Delta Breakout

Among the three legacy carriers, American Airlines and United Airlines have traded dominance for the better part of two years. On an overall average basis, American holds the highest share of legacy group engagement in the 17–25 age bracket (~40%) and the 36–45 bracket (~43%), while United leads the most valuable segment of 46+ at roughly 39%.

But the most recent quarters point to a meaningful shift. Within the 17–25 cohort, leadership has seesawed between American and United since Q1 2024. American surged to 52% of the legacy group’s young-adult engagement in Q2 2025, its high-water mark in the dataset. That share has since dropped in three consecutive quarters, falling to roughly 26% by Q1 2026. Delta, which hovered around 22–26% of the legacy group’s 17–25 share through mid-2025, has moved in the opposite direction, climbing to 36% in Q4 2025 and then to 39% in Q1 2026, making it the leader among legacies in the youngest cohort for the first time in the studied period. Delta simultaneously took the top position in the 26–35 group at 39%, also a first.

“The Delta move in the 17–25 cohort is worth watching,” said Tom Grant, VP Research at Apptopia. “Young travelers may be picking a loyalty program, not just a flight. If Delta is gaining that cohort at American’s expense, the compounding effect on SkyMiles enrollment and lifetime revenue could show up in the financials two or three years from now. The 46+ rotation from United to American is the other thread to pull on because those are the premium cabin buyers. When leadership changes hands there and holds for three consecutive quarters, that’s a signal.”

The 46+ segment has seen its own inflection. United led that cohort within the legacy group for six of the first seven quarters tracked, peaking at 45% share in Q1 2025. Beginning in Q3 2025, however, American Airlines overtook United and has held the lead for three consecutive quarters, most recently at 37% versus United’s 35%. For investors tracking customer lifetime value in the highest-engagement demographic, that handoff may matter.

The LCC/Hybrid Market: Southwest’s Commanding Lead

The competitive picture among low-cost and hybrid carriers looks nothing like the legacy race. Southwest Airlines is not just leading and dominating. Across the full period, Southwest holds approximately 72–75% of the group’s sessions in the 36–45 and 46+ age brackets, and 69% in the 26–35 cohort. Among 17–25 year olds, its share of the LCC/hybrid group reached 85% in Q1 2026.

JetBlue and Alaska Airlines occupy a distant second and third, and neither has led any age segment in any quarter over the entire two-year period. JetBlue’s strongest relative position is in the 26–35 bracket, where it held roughly 22% of the group’s share in Q1 2026. Alaska Airlines shows a similar footprint in the 26–35 bracket at 26%, its highest mark. But in the youngest cohort both carriers have all but disappeared, combining for just 15% of the group’s share in Q1 2026.

The implication is clear: within the LCC and hybrid tier, Southwest has effectively consolidated the market. The question for JetBlue and Alaska is less about overtaking Southwest and more about whether they can carve out a defensible niche at all.